![]()

S. Hampton Roads equity gains may outweigh sub‑3% mortgage benefits, even as Virginia’s rate‑lock effect remains stronger than national trends.

VIRGINIA BEACH, VA, UNITED STATES, July 7, 2026 /EINPresswire.com/ — The widely cited “3% mortgage lock-in effect” has become a defining explanation for today’s subdued housing turnover nationwide. But in South Hampton Roads, rising home equity is adding a second force that may be reshaping that narrative in subtle but important ways.

New analysis from Virginia Beach REALTOR® Liz Schuyler of RE/MAX Allegiance finds equity built since 2020 may now outweigh the financial benefit of holding a 3% mortgage rate — a reversal of the assumption driving most national housing coverage this year.

While low mortgage rates continue to discourage some homeowners from selling, a separate dynamic—rapid equity accumulation since 2020—is increasingly influencing mobility decisions in the region.

“Homeowners often fixate on their interest rate but rarely measure their equity,” said Liz Schuyler, REALTOR® with RE/MAX Allegiance. “Rates matter, but equity can reshape the entire decision and reveal options many don’t realize they have.”

A National Milestone, and a Virginia Rate Picture:

As rates have risen, the Federal Housing Finance Agency (FHFA) National Mortgage Database has found that the predominance of the under 3% rate bucket and the 6%+ rate bucket have swapped places within the past year. In Q1 2025, mortgages below 3% still outnumbered those at 6%+, 20.5% to 18.9%. By Q1 2026, that had flipped: 22.1% of mortgages now sit at 6% or higher, versus just 19.5% below 3% — and that reversal has held. This national shift sets the stage for understanding why Virginia stands out even more.

FHFA’s own national and regional breakdowns for Q1 2026 show Virginia is an outlier — not just against the nation, but against its own region. And within that national shift, Virginia bucks that trend entirely: 22.9% have mortgage rates below 3% and 20% have rates 6%+. Virginia also shows a higher share of sub‑5% mortgages — 68.9% compared with 66.7% nationally. The state sits well above its own region on all counts, plausibly tied to longer tenure and a large base of military families who bought and stayed through PCS cycles rather than trading up.

That makes Virginia’s lock-in effect stronger than the national or regional numbers suggest — exactly why the equity math matters more here, not less.

What the Local Numbers Show:

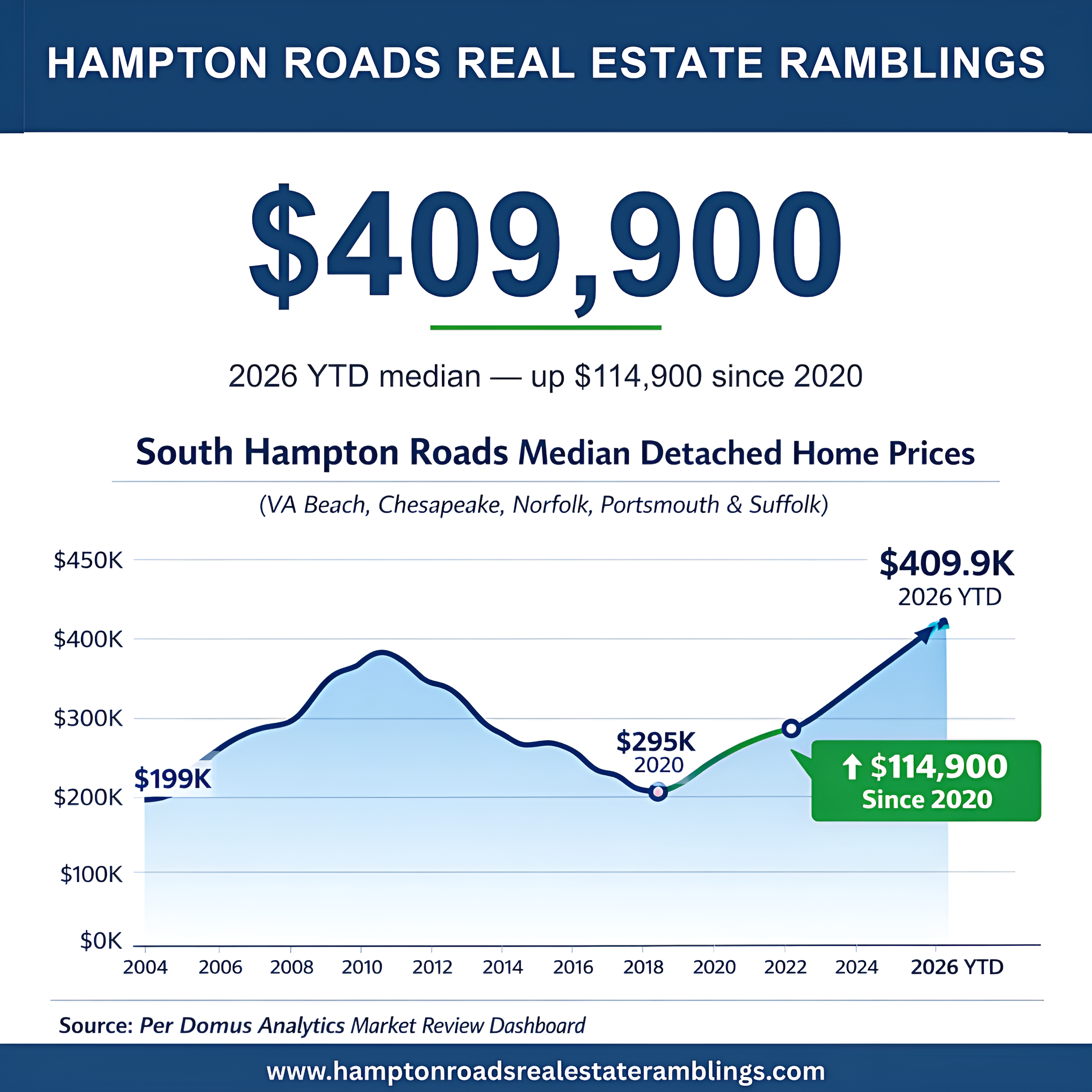

Since 2020, home values in South Hampton Roads have risen steadily, driven by limited inventory and sustained demand. Based on regional MLS and market tracking data, median detached home prices across Virginia Beach, Chesapeake, Norfolk, Portsmouth, and Suffolk have increased from roughly $295,000 in 2020 to about $409,900 in 2026 year-to-date.

That represents more than $100,000 in median price appreciation over six years, significantly increasing owner equity for households that purchased before or during the early stages of the pandemic housing cycle. That sustained appreciation reduces the amount of financing required for a subsequent purchase and partially offsets the impact of higher mortgage rates.

Schuyler says, “For many long‑term owners, the question is no longer simply ‘Should I give up my rate?’ but ‘What does my equity now allow me to do?’”

A Market Shaped by Two Competing Forces:

The emerging regional dynamic can be described as a tension between two forces:

• Financing constraint: Higher mortgage rates discourage selling by increasing replacement housing costs

• Equity expansion: Rising home values increase net worth and potential down payment power

In much of the country, the first force dominates. In South Hampton Roads, however, sustained price appreciation has strengthened the second.

This does not eliminate the lock-in effect, but it may narrow its influence for certain segments of homeowners—particularly long-term owners with significant equity positions.

A More Nuanced Decision Framework Is Emerging:

Rather than relying on a single-factor “rate lock-in” model, housing decisions in the region increasingly reflect a combined assessment of equity, real payment differences, life circumstances, and the cost of staying put.

For more information see “Should You Give Up Your 3% Mortgage?” A Hampton Roads Homeowner’s Guide to Making the Right Move

The Bottom Line:

The “3% mortgage” narrative remains an important explanation for reduced housing turnover. But in South Hampton Roads, sustained appreciation over the past several years has created a growing cohort of homeowners whose equity positions materially change the calculus.

For these households, the decision is less binary than it appears in national headlines. The question is not only what is being given up in interest rates, but what accumulated ownership value may now enable. Schuyler provides customized equity analyses to help homeowners understand how their current position compares to today’s market conditions — and whether a move may be more feasible than expected.

Liz Schuyler

RE/MAX Allegiance

+1 757-235-0274

liz.schuyler@gmail.com

Visit us on social media:

Facebook

Other

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery